The wine sales of the Finnish monopoly Alko are shrinking by no accident

“We’re on a road to nowhere,” sang the Talking Heads in 1985 — and uncomfortably, the line fits Finland’s wine monopoly in 2025 rather well. As Alko’s sales volumes fall by double digits and nearly half of the lost liters resurface in grocery stores after the 8 % reform, the market isn’t stabilizing — it’s drifting. What looks like a downturn is in fact structural erosion: consumption is fragmenting, loyalty is thinning, and the monopoly’s foundation is being tested in real time.

The 8 % Reform Exposed a Structural Weakness

Let’s stop calling this a downturn (In 2024–2025, Finland reformed its alcohol legislation by raising the maximum alcohol content of beverages sold in grocery stores from 5.5 % to 8 % ABV.) What happened to wine sales inside Alko in 2025 is not due to cyclical softness, seasonal fluctuation, or consumer mood, but rather structural erosion — and the 8 % grocery reform merely exposed how fragile the monopoly’s wine model had already become.

Between January and October 2025, Alko lost a staggering 3.7 million liters of wine sales, a drop of –10.5 % compared to the same period in 2024.

At the same time, grocery stores increased sales of wine-based beverages by 1.8 million liters, a dramatic +39.3 % surge. Almost half of Alko’s lost volume instantly reappeared in supermarkets and it is not a coincidence, but a substitution. (Stats by LVV)

The Consumer Didn’t Disappear, Merely Walked Next Door

For decades, the monopoly model depended on friction. If you wanted stronger wine than grocery beer limits allowed, you went to Alko, made a separate trip, and accepted limited opening days and hours. Whence, you had to plan your purchase beforehand.

However, the 8 % reform changed that equation; low-alcohol wine-based beverages could sit in the same basket as milk and pasta. So, they became impulse purchases. Nowadays they are integrated into everyday shopping behavior.

The reform did not create any new demand, it only removed the purchasing friction. Once friction disappeared, the true elasticity of consumer loyalty became visible. As a result, nearly half of Alko’s volume loss transferred immediately to groceries. If that does not cause concern to anyone believing that the monopoly structure is inherently stable, then nothing else will.

The Reform Is Only Half the Story

Even after accounting for the 1.8 million liters that migrated to grocery retail, roughly 1.9 million liters of wine simply vanished from the system.

This hints at a second, more uncomfortable reality: Finns are drinking less wine.

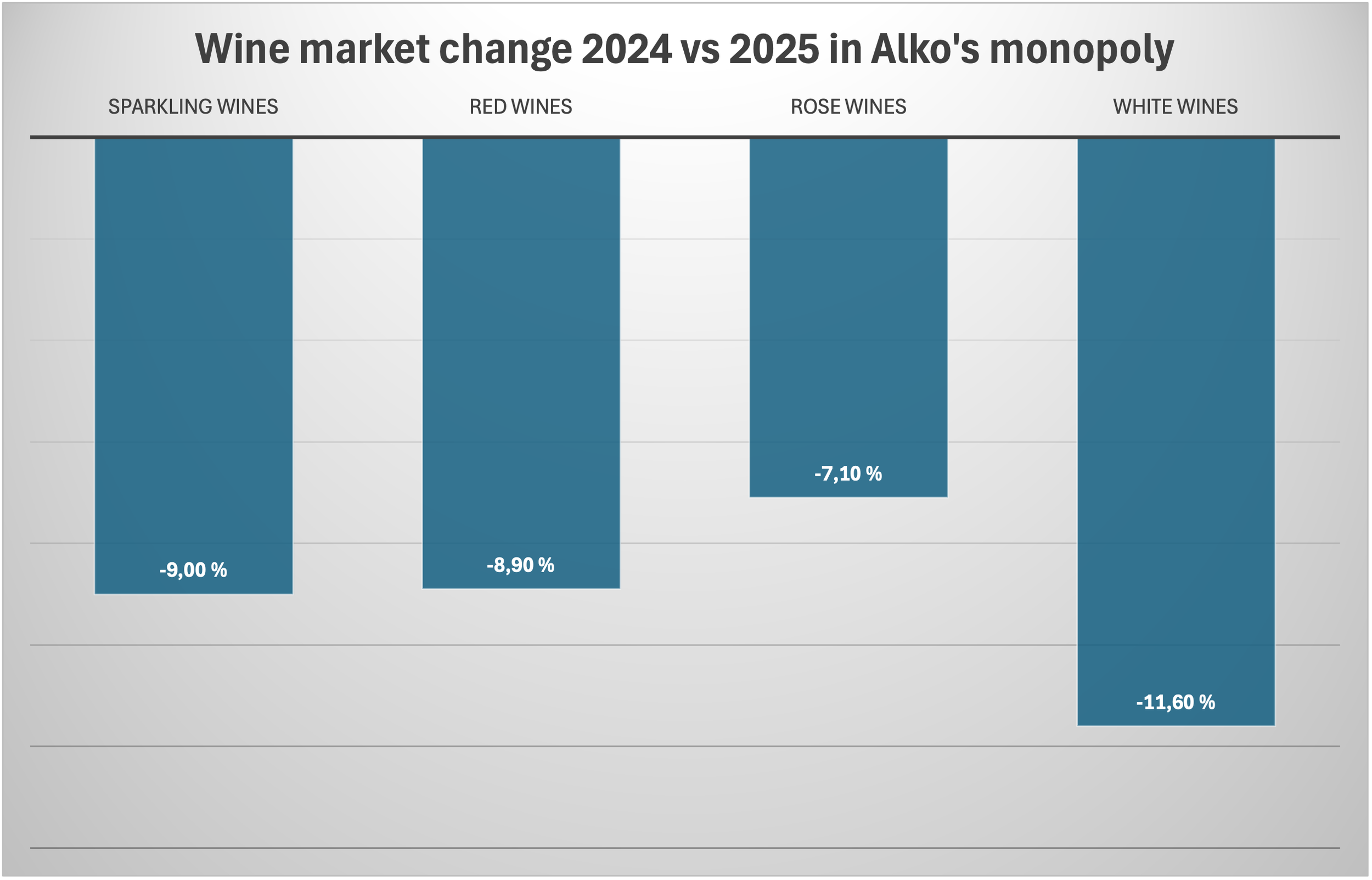

Source: Alko sales statistics

White wines fell –11.6 %.

Red wines –8.9 %.

Sparkling –9.0 %.

Rosé –7.1 %.

White wine — the largest segment at 42.8 % market share — declined the most. As the backbone of consumption weakens, it is not due to mere stylistic change.

There are many possible factors at play. The younger demographic drinks less and less alcohol, health awareness is rising as a whole, non-alcoholic alternatives are improving and due economic slump the price sensitivity has increased. The fact is that the monopoly did not cause these trends, however, it is uniquely vulnerable to them.

The Monopoly Magnifies Decline

In open retail markets, falling demand can be met with rapid portfolio shifts, aggressive pricing, innovation and marketing. In a centralized monopoly system, listings are bureaucratic, portfolio changes are slow and recovery depends on institutional adjustment rather than competitive agility. So, when consumption declines, this structure amplifies the sales decline. Country-level sales statistics by Alko reveal just how brutal the amplification can be.

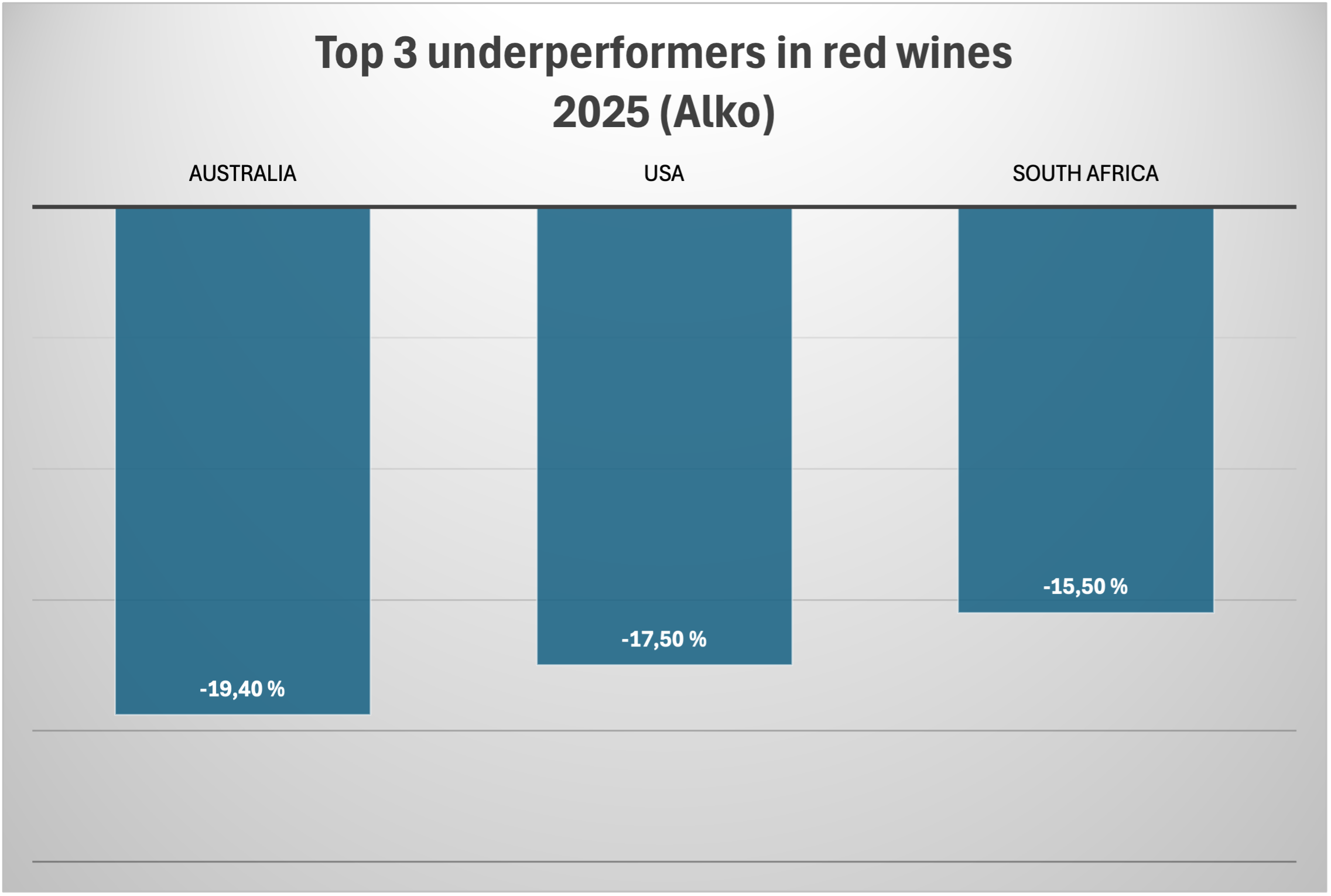

Source: Alko sales statistics

Red wine losses:

● Australia –19.4 %

● USA –17.5 %

● South Africa –15.5 %

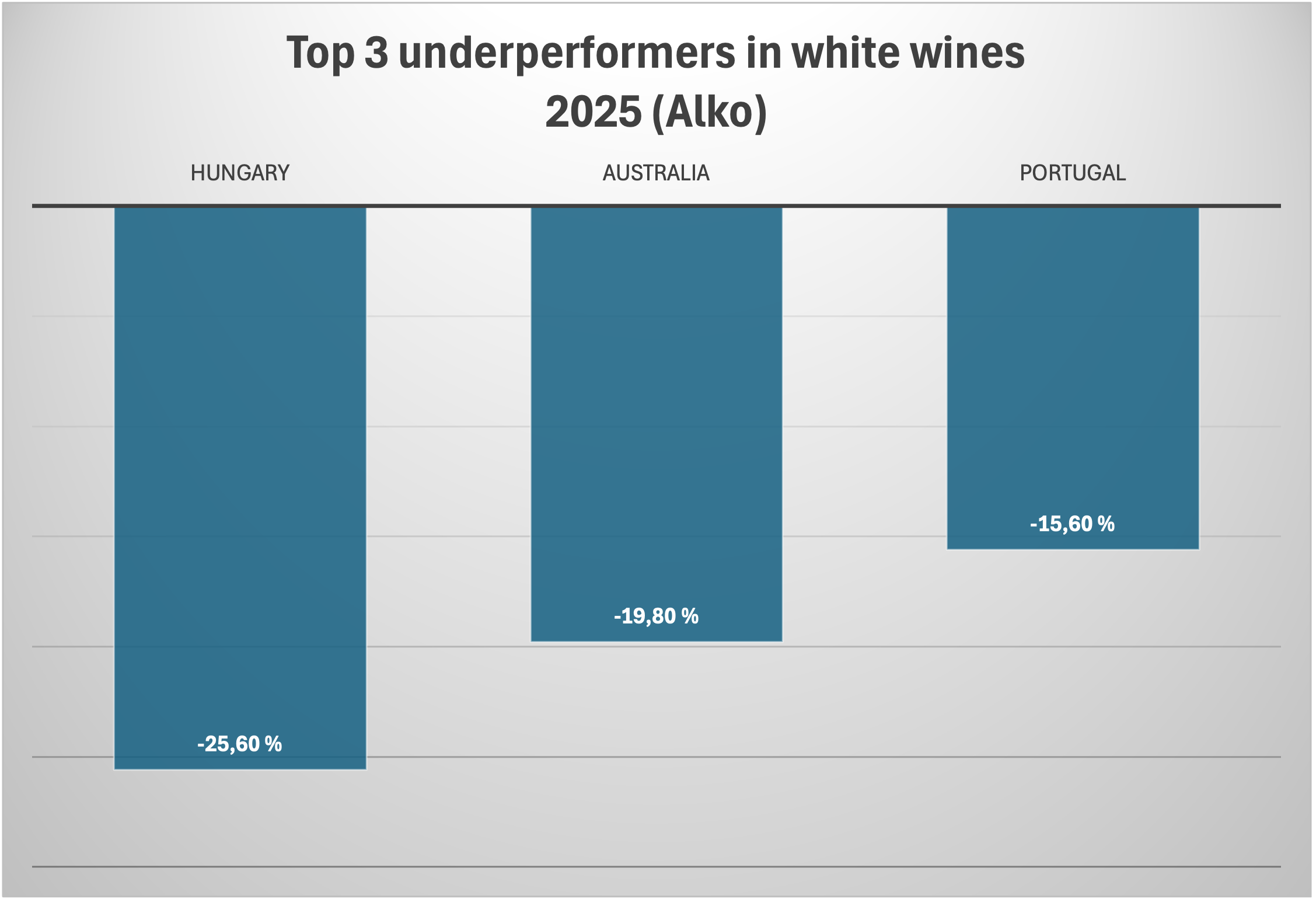

Source: Alko sales statistics

White wine losses:

● Hungary –25.6 %

● Australia –19.8 %

● Portugal –15.6 %

These are not minor corrections, they are major losses and can be described as market collapses.

The Illusion of Stability

The defenders of the current system argue that overall alcohol consumption is falling everywhere in Europe. This may be partially true, however, it is not commonplace for nearly half of lost volume to reappear instantly in grocery stores after a modest regulatory shift.

That is the monopoly's systemic vulnerability in plain sight and it can not be explained by demographic inevitability. The 8 % reform did not destroy the monopoly’s wine market. It only demonstrated how much of it was dependent on regulatory exclusivity rather than consumer preference.

A Dangerous Economic Equation

Here is the uncomfortable question:

can a nationwide monopoly structure which is built on a volume scale remain economically stable, if said volume steadily erodes? If grocery limits eventually expand beyond 8 % and the internet sales are written to the Finnish alcohol law (albeit already legal in EU), the 2025 shift may begin to look modest in hindsight.

The risk associated is not an immediate collapse, rather slow evaporation. First the volume begins to decline while fixed infrastructure remains and margins begin to tighten. Shortly after, the political scrutiny would increase. Once this structural contraction becomes embedded, reversing it is far harder than preserving it.

Survival of the Fittest?

The debate is no longer about whether wine consumption is falling. It is about whether the current monopoly architecture is resilient to market fluctuations in a dual-channel environment. Finland now operates in practice with two wine markets: grocery stores — offering convenience, lower alcohol, special offers — and Alko, which in turn offers stronger alcohol, premium and curated. The 2025 data (Alko 2025 sales statistics) shows the first wave of redistribution. Question is, whether the monopoly can adapt before the next regulatory shift exposes another layer of structural vulnerability. It is not up to debate whether Alko’s numbers suggest stability, they suggest a major fragility.